How to Effectively Manage Your Home Loans and Budget Accordingly?

A home is your family’s identity, symbolic of your legacy! Owning a house is the ultimate goal, and home loans are the catalysts for first home investment.

Here are a few tips before taking home loan–

Create a blueprint of your monthly finances

Income

- Monthly salaries

- Returns on investments

- 2nd source

- Government incentives (if any)

Investment

- PPF

- CAGR and reinvestment

- Retirement schemes

- Shares/bonds/mutual funds

Expenditures

- Fixed

- Rent

- Mortgage payments

- Insurance

- Miscellaneous debt: student loans, personal loans etc

- Utilities (electricity, gas, water, etc.)

2. Variable

- Groceries

- Commute

- Entertainment

- Healthcare

- Credit card bills

| Property investment guide Tobuy property in Pune, you need to follow a basic rule of thumb for managing your finances: 50-30-20 Out of all your expenses, 50% of the inflow should be dedicated to essentials.30% of the monthly budget should be allotted to the wants. (This is variable, so it is advised to make adjustments here if you are planning on investing).For more conducivehome loan tricks and tips, 20% of your monthly savings should be set aside for loan repayments. |

The power of down payment

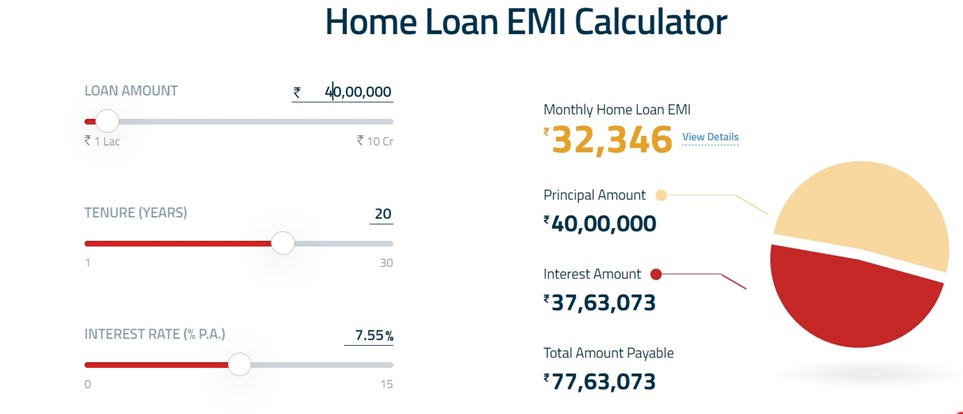

One of the most lucrative home loan tips is to put a maximum amount as a down payment. Say you want to buy a home in Pune, and you have availed a home loan from a bank. According to RBI regulations, banks can issue only 80% of the property value, which must be over INR 30 Lakhs. The rest of the payment is considered a down payment a buyer pays. Let us consider two scenarios:- The total property value is INR 60 lakhs.

Scenario #1

In this case, you have put a down payment of Rs 20 Lakhs, i.e. 33.33% of the total value.

So, now your principal amount of loan becomes Rs 40 Lakhs.

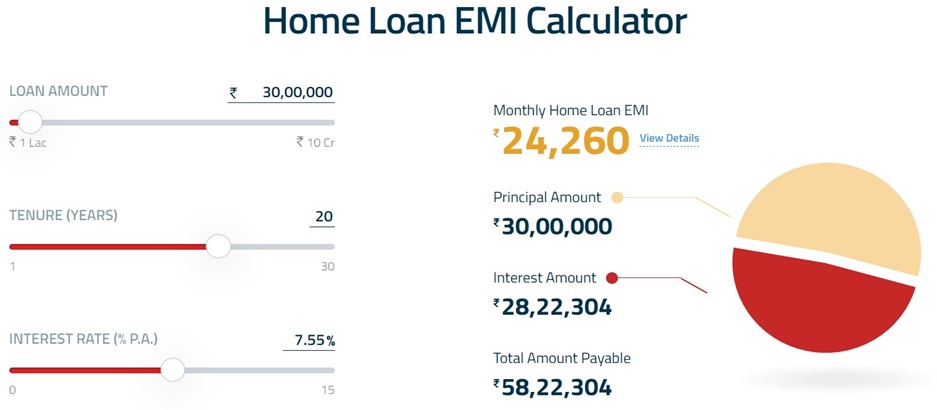

Scenario #2

Whereas in this case, you have already put a down payment of Rs. 30 Lakhs, i.e. 50% of the total value of property in Pune. Now, the remaining Rs.30 Lakhs is the principal amount.

| Key Inferences: With the interest rate and tenure constant, you notice a significant difference between the total interest payable. Since the principal amount is lower in 2nd case, you can easily adjust the EMIs in a lesser tenure. Overall, putting down a large initial payment relieves the burden of loan repayments. |

Selecting a suitable EMI plan

The next step is to evaluate your EMI. The primary factor affecting these instalments is the term of the loan.

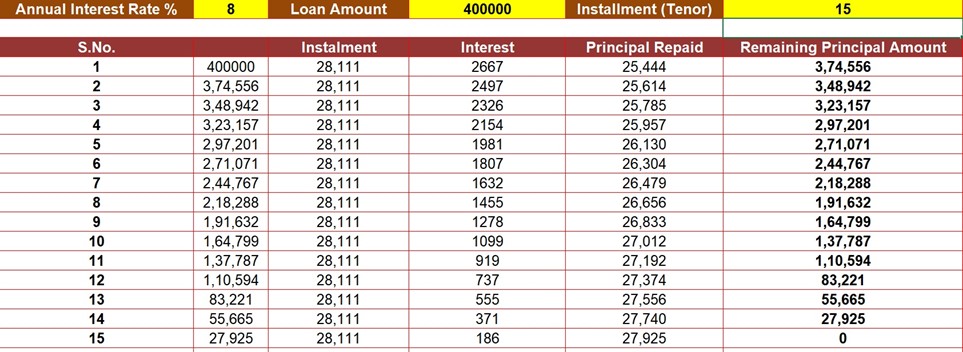

Scenario #1

Here the loan amount is Rs.40 Lakhs, and the tenor is 15 intervals.

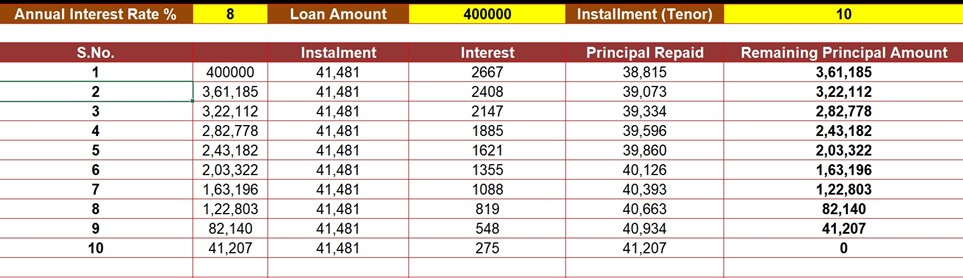

Scenario #2

The loan amount is the same but the tenor is reduced by 5 intervals.

| Key Inferences: Even though the instalment is considerably lower in the 1st case, if we tally throughout the tenure, you pay Rs.421665 in 15 instalments, while you pay only Rs.414810 in 10.The difference in the interest column— Rs.21664 in the 1st case while paying only Rs.14813 in the 2nd case. Hence, paying off your loan with a lesser tenor is recommended, yielding better ROI on real estate since the interest paid is lower. |

What kind of interest rates should you opt for?

The home buying process has a long-term ripple effect on your personal finances. These rates are basically the cost of applying for a home loan.

Floating Rate

Also known as ‘adjustable rate’, this rate “floats” according to the market movement.

EMI amount– with floating rates, the EMI amounts can be lower for certain months depending on the market.

Reducing the tenure– you can pay an extra EMI for the months with a lower rate.

Fixed Rate

With a regular steady income, this rate is suitable if you are comfortable with the EMI amount. According to one of the most recommended home loan repayment tips– your EMI must not exceed 25-30% of your monthly income.

| If you can’t decide which one to choose, you can always opt for flexible plans by banks that offer fixed interest for initial years and then change it to a floating rate with some nominal fees. |

Credit Score will make you a “man of the match”

If you want to optimise your home loans, the best way is to maintain your CIBIL score above 750-800. This will reward you with lower interest rates than usual. High credit scores also yield instant loan approvals.

PRO TIP: Home Loan under woman’s name

To encourage women to invest in real estate, the government has issued several policies that can optimise your savings.

- Lower interest rate: special home loan interest rates are levied that are a few points lower than the general rate. Whereas the subsidised rates are 0.05-0.1% lower, thus saving considerably in EMIs.

- Reduced stamp duty: most states are offering 1-2% lower stamp duties on the property for women than the actual levied.

- Tax benefits: both husband and wife as co-owners can claim tax deductions where women can enjoy the benefit of tax deductions of— a maximum of Rs 2 lakh on interest repayment and Rs 1.5 lakh on the principal amount.

Properties in Mumbai and Pune are residential hotbeds— offering various career opportunities, a robust security system, the best healthcare facilities, top-tier educational institutes, and progressive infrastructure. Utilise these tips to secure your dream home!

FAQs:

Q1: Do I have to pay a fixed amount for my EMI?

A: Equated monthly instalment is a predetermined value based on the principal amount and interest rate. But you can make an extra EMI payment within a month.

Q2: Can I just cancel my loan?

A: You can cancel it only before the amount is disbursed.

Q3: Why do I need Income proof for applying for a home loan?

A: An income proof indicates the ‘creditworthiness’ of a person, assuring the lender of repayment.

Q4: Do I need to visit India to apply for loans as an NRI?

A: It is not necessary to visit India if you have a co-applicant or GPA (general power of attorney).

Q5: Can I miss an EMI payment?

A: It is advised to maintain a disciplined payment to avoid a lower credit score.

Q6:What are the options available in selecting loan tenure?

A: You can select somewhere between 5-30 years, depending on your age.